DCK Investor Edge is a weekly column about investment in the data center market, covering both publicly traded data center REITs and privately held players in the space. More about the column and its author here.

Investing in long-term growth can be a mixed bag for a publicly traded company. The stock market will often punish a company in the short run if a smart move does not increase earnings – something Iron Mountain experienced for itself last week, after it announced its $1.3 billion acquisition of Phoenix-based IO Data Centers, expected to close early in 2018.

The IO deal will be the largest investment the company best known for its global document storage and data management services has made in data center colocation, disaster recovery, and cloud services. Iron Mountain has removed any doubt that management is serious about growing its data center business and growing it quickly.

But it takes a lot of capital to own and operate data center real estate, and the question Wall Street investors are now pondering is how long IRM data centers will take to pay dividends.

Small Steps at First

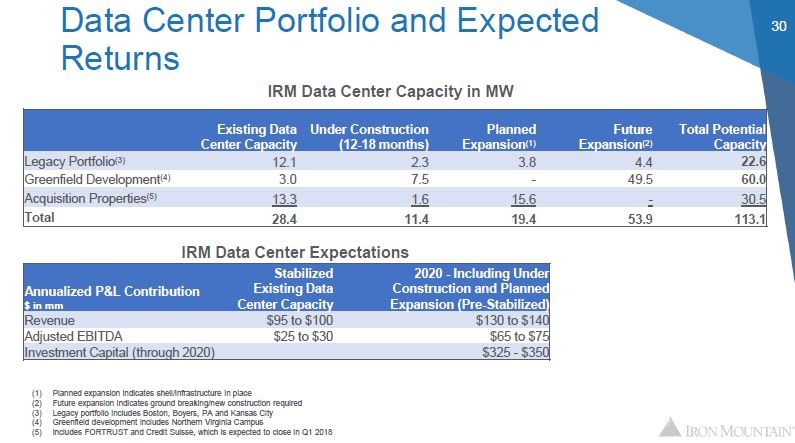

Last year, Iron Mountain garnered headlines with the announcement of its first major data center development in Northern Virginia. It was a measured and conservative move. The company is planning to develop the 83-acre parcel in Manassas in four stages, which together can yield 62MW of data center capacity. The first 10.5MW data center shell was completed this fall, its initial 3MW phase 50 percent leased at launch.

Earlier this year, it closed on the $128 million acquisition of Denver-based Fortrust, adding to its portfolio a 210,000-square foot colocation data center serving 250 customers. This added 9MW, bringing Iron Mountain's total data center capacity to 30MW and potential to build out another 70MW.

In October, Iron Mountain announced its first international data center acquisition: the sale-leaseback of two Credit Suisse data centers in London and Singapore totaling 14MW. Credit Suisse agreed to lease 4.2MW back as the anchor tenant after the $100 million deal closes early next year.

In the November NAREIT presentation slide above management detailed a methodical approach, with conservative guidance of $325-$350 million for planned investments through 2020.

Why Did IRM Shares Sell Off?

Iron Mountain is a real estate investment trust that has attracted investor interest due to its ability to generate earnings growth both organically and through M&A -- supporting a growing dividend.

The IO deal adds a new wrinkle to the mix. The much larger than anticipated acquisition will initially be dilutive to existing shareholders. Iron Mountain is funding it through $825 million in debt and an offering of 16.675 million secondary shares (including underwriter option) at $37.00 per share.

The announcement resulted in a sharp sell-off for IRM shares, sending them down 7.1 percent on the first trading day after the announcement:

Moody's rating agency changed its Iron Mountain rating to Ba3 negative from stable (based on balance sheet leverage concerns).

Before last week’s drop, Iron Mountain had been outperforming a strong S&P 500 throughout the year. The shares, which were previously trading at $40.70, had racked up a gain of 23 percent in addition to the healthy 6.25 percent dividend, paid quarterly. All this is to say that at least in the short term, IO appears to have been an expensive acquisition.

IRM Data Center Strategy

But that’s not the whole story regarding this transaction, according to Mark Kidd, senior VP and general manager for Iron Mountain Data Centers.

The company expects the deal to provide a major boost to its near-term and long-term growth projections, Kidd said in an interview with Data Center Knowledge. He estimated it will add 2 percent in revenue and 3 percent in EBITDA. "When you start to see that kind of growth with the committed four percent dividend increase per year, I think the story actually starts to become pretty compelling; and that’s how we look at it," he said.

Kidd also discussed the conservative financial modeling and guidance given to Wall Street for the data center business and confirmed that all data center acquisitions were underwritten to be accretive in the second year of operation.

He pointed out that the data center business investments will accelerate adjusted EBITDA growth, which will naturally help to delever the balance sheet.

Graduating From “Adjacent Businesses"

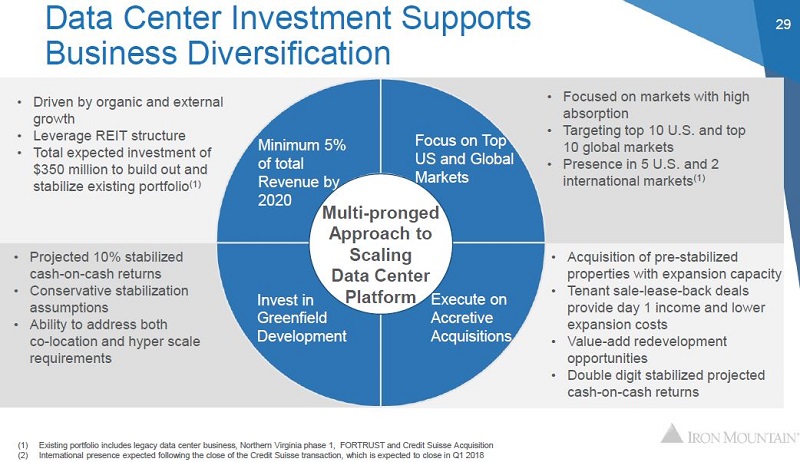

Iron Mountain CEO William Meaney said in the announcement last week that adding IO's US operations would "accelerate our growth profile by bringing our data center business to approximately 7% of total revenue and approximately 10% of Adjusted EBITDA by 2020 – significantly exceeding our initial goal – while enhancing business diversity and the margin profile of the company."

Historically, diminimus revenues from Iron Mountain data center operations were lumped into Adjacent Businesses, an accounting bucket that includes things like fine art storage. The stated goal over the past few years has been to grow these businesses to 5 percent of total revenues by 2020 – including colocation data centers, Iron Cloud, and disaster recovery. Magnetic tape storage and services are reported in Data Management and account for 14 percent of revenues.

Kidd confirmed that after the IO transaction closes in early 2018, Data Centers will be broken out as a line item. This should give investors more clarity regarding pace of organic growth, re-leasing spreads, customer churn, and new logo signings.

Data Center Growth Challenges

Secular drivers for global data center revenue growth have never been stronger. The success enjoyed by both publicly traded and privately owned data center operators has attracted enormous amounts of capital looking to invest in this red hot sector.

The competition to acquire quality properties and data center franchises continues to drive up valuations, with many transactions during 2017 priced at 13x-19x EBITDA, or even higher. This can make it challenging for public companies to show immediate earnings accretion unless they have a hoard of cash to invest, an investment grade balance sheet, or shares trading at earnings multiples considerably higher than the targeted acquisition.

IRM shares trade at about 12.8x consensus 2018 AFFO -- a much lower multiple than its pure-play data center REIT cousins which trade in the mid-20s. Iron Mountain shares are priced lower in-line with the growth prospects of its core document storage business which explains why the IO acquisition is dilutive.

Investor Edge

Iron Mountain is an S&P 500 company with close to $4 billion in annual revenue. Therefore, scaling the data center business requires a significant M&A component in addition to the Northern Virginia development and organic revenue growth off a relatively small base.

The Fortrust acquisition and the pending IO deal give Iron Mountain scale and immediate operating leverage, adding 250 and 550 colocation customers, respectively. Fortrust in the Denver market, and IO mainly in Phoenix, where it has been expanding in one of the fastest growing US data center markets (an important consideration, according to Kidd). Additionally, the IO facility in Edison, New Jersey, when combined with the London and Singapore Credit Suisse data centers, will help Iron Mountain compete for financial services customers.

Today, the company’s management finds itself between a rock and hard place. Scaling a data center business requires biting the bullet in the stock market in the short term. However, in a few years, Iron Mountain will have the option of spinning out the faster growing data center business and rewarding the patient shareholders.