If the Switch IPO proceeds as planned, SWCH shares will be traded on the New York Stock Exchange. The Las Vegas-based company has filed documents to go public, hoping to become the sixth major US-based publicly traded data center provider, joining Equinix, Digital Realty Trust, CyrusOne, CoreSite, and QTS Realty. Iron Mountain is another publicly traded data center provider, but it's one of several businesses the company is in.

The Switch IPO, which if successful may become the third-largest tech IPO this year, gives investors in data center stocks another opportunity to buy shares of a smaller-cap, growth-oriented colocation and wholesale data center operator. The company provides both super-wholesale and retail colocation and interconnection options, setting it apart from 100 percent wholesale-focused DuPont Fabros Technology (now operating as part of Digital Realty).

Goldman Sachs, J.P. Morgan, BMO Capital Markets, Wells Fargo Securities, Citi, Credit Suisse, and Jefferies are the joint bookrunners on the deal expected to price next week, according to IPO expert Renaissance Capital.

The Big Picture

The deal has plenty of exciting aspects for investors to consider. I highlighted those in a DCK Investor Edge column earlier this month, in the first part of our Switch IPO coverage: The Unique Proposition of a Switch IPO

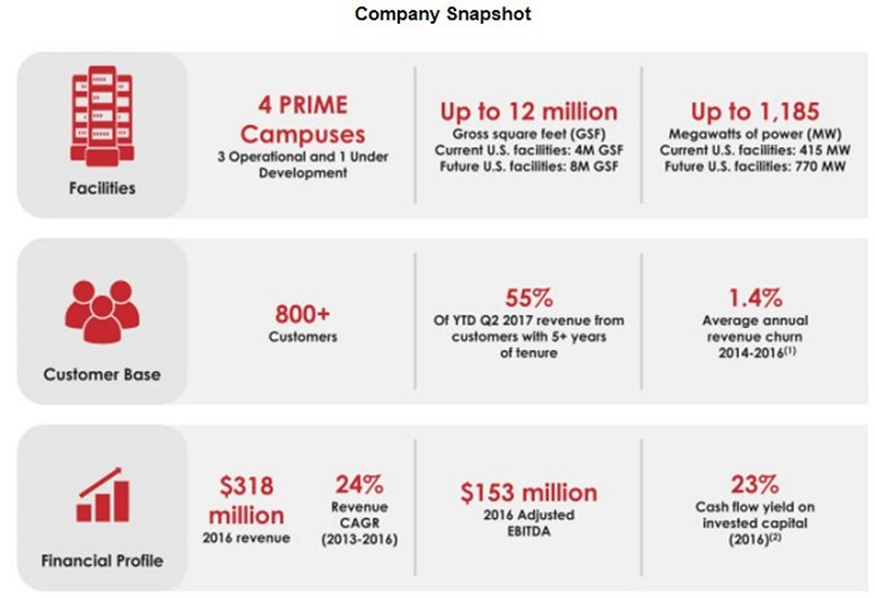

The graphic below is from the Switch IPO Prospectus dated September 27, 2017. It highlights the facilities, customer base, and curated financial metrics.

Switch - company snapshot

What it does not highlight is the fact that Switch derives almost all of its revenue from its Las Vegas campus -- a form of concentration risk.

Concentration Risks

According to the company:

Our data centers located in Las Vegas comprised 95.8% of our revenue during the six months ended June 30, 2017 and comprised 99.4% of our revenue during the year ended December 31, 2016. The occurrence of a catastrophic event, or a prolonged disruption in this region could materially and adversely affect our operations.

While it has more than 800 customers, eBay is the largest, accounting for 9.6 percent of annual revenue. There were no details of eBay leases in the prospectus. The top 10 Switch customers accounted for approximately 38.4 percent and 38.1 percent of revenue for the year ended December 31, 2016 and the six months ended June 30, 2017, respectively.

That said, all data center operators that provide massive data halls leased to super-wholesale customers on long-term leases have tenant-concentration issues baked into the cake. Under the right circumstances (especially when tenants are considered investment-grade), this can be viewed as a good problem to have.

In addition to wholesale deployments, Switch incubates a bevy of smaller tenants in its retail colocation operations and can reap the benefits when they land and expand. The prospectus points out that some US federal, state, and local government tenants "may terminate all or part of their contracts at any time, without cause."

Business Risks to Consider

Investors considering adding Switch shares to their portfolios may want to consider some of the risks associated with how the business is structured:

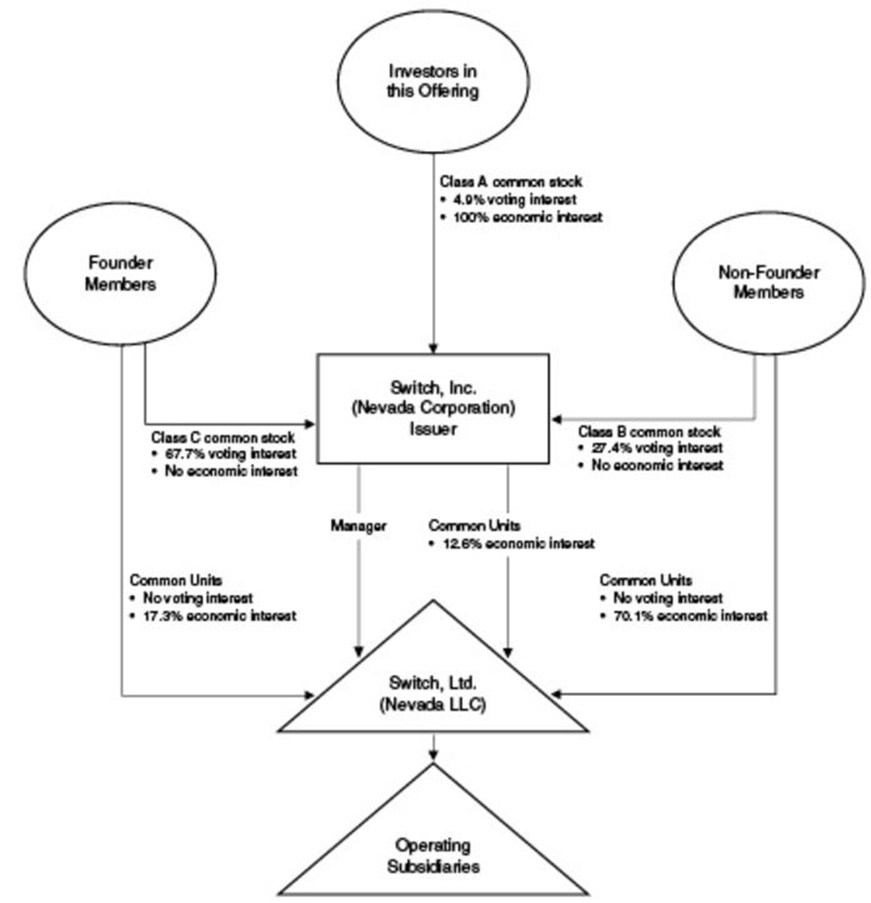

Source: Switch, Inc. Sept 25, 2017 S-1 filing

Management: A lack of normal checks and balances of an independent board of directors. The board appointments are controlled by founder, CEO, and chairman Rob Roy, primarily through a 10-to-1 voting preference for his Class-C shares, in addition to his partnership units. Roy would be in complete control of Switch, Inc. after the IPO. (p.43 of the prospectus)

Man of Mystery: Roy's biography on the Switch website gives little insight into his professional background prior to Switch in 2000 or his formal education. The prospectus bio does not shed any additional light on the 48-year-old founder. (p.140)

However, Roy has been prolific when it comes to innovation and patents. "The designs of our data center facilities are protected by over 350 issued and pending patent claims documenting inventions by Rob Roy." (p.121),

Dividends: Switch, Inc. is not a REIT. Dividend policy, if any, is up to the board. Switch's publicly traded peers are all REITs, and pay regular quarterly dividends. Assuming this would automatically be the case with Switch would be incorrect. (p.55), (p.64)

Notably, management's Class-B shares, Class-C shares, and Member Common Units would not be eligible for dividends if any are declared.

Dilution: Assuming the 4.68 million underwriter "greenshoe" is exercised in full, book value of Class-A common shares purchased for $15.00 would be $2.58 per share immediately after the IPO is completed.

The 31.25 million Class-A shares being sold to the public at an estimated $15.00 IPO mid-point would represent just 12.6 percent of the total shares when the 215.8 million Class-B, Class-C, and Member partnership units are taken into consideration, as shown above. (p.68)

Notably, in addition to Switch management and board members, Intel Capital Corp. owns 5.3 percent of Class-B shares. (p.166)

Controlled Company: "Upon completion of this offering, the Founder Members will control more than 50% of our combined voting power. As a result, we will be considered a ‘controlled company’ for the purposes of NYSE rules and corporate governance standards." (p.47)

Use of Funds: "The Tax Receivable Agreement with the Members requires us to make cash payments to them in respect of certain tax benefits to which we may become entitled, and we expect that the payments we will be required to make will be substantial." (pp.42-44), (p.63)

It is difficult to estimate how this will impact the Switch, Inc. cash flow, and how much it will impact the bottom line.

Encumbered Assets: "Our credit facilities are secured by a first-priority security interest in substantially all of the assets of Switch, Ltd. and its wholly-owned material domestic subsidiaries." (p.27), (p.179)

Leased vs Owned: "Two of our facilities and one of our facilities under development are located on properties for which we have long-term operating and capital leases. We also lease the building shell for one of these facilities. Such leases generally have remaining terms of 15 to 49 years." (p.37)

This list is not intended to be comprehensive. These are just highlights. The information above should be examined along with the entire S-1 Prospectus filing. The page numbers are intended to be used as "footnotes" and a guide to help with investor due diligence.

Investor Takeaway

The secular drivers of cloud computing, wireless data, streaming video, big data, AI, IT outsourcing, and the Internet of Things certainly make data center stocks appealing – perhaps even exciting at times.

There have been multiple data center M&A deals, major property acquisitions, and a surge in private equity investing activity this past year. This underscores how institutional investors are trying to find ways to participate in sector growth and strike it rich with a data center bonanza.

The Switch intellectual property, resilient designs, impressive customer list, 100 percent green energy, and unique data center geographic footprint all combine into an exciting story. However, there are some unusual aspects of the Switch, Inc. IPO prospectus, especially those involving corporate governance and alignment of management with Class-A shareholders.

This makes an early investment in Switch potentially riskier than just buying shares in the five publicly traded data center REITs. These REITs have a track record of growing earnings (FFO/AFFO) per share and paying regular dividends.

Investor Edge

Frankly, any investing can be viewed as risky business. It is up to each investor and their advisors to weigh IPO risks against the potential rewards of investing with the visionary founder of one of the most innovative data center businesses on the planet.

According to Fidelity:

IPOs can generate buzz among investors, particularly for so-called 'hot issues' that garner a lot of interest. But beware of getting caught up in the hype: IPO investing can be complex and may be suitable only for experienced investors. Be sure to consider any opportunities within the constraints of your unique investment goals and risk tolerance.