DCK Investor Edge is a weekly column about investment in the data center market, covering both publicly traded data center REITs and privately held players in the space. More about the column and its author here.

The CyrusOne $442 million acquisition of European wholesale data center provider Zenium, announced in late December, was an exciting way to end a record year for data center mergers and acquisitions.

Upon closing of the transaction CyrusOne will join Equinix and Digital Realty as the third publicly traded US-based data center operator with significant customer offerings in both North America and Europe.

In addition to 27 MW of leased space and Zenium’s deal pipeline, CyrusOne will immediately gain 22.5 MW of powered shell inventory to offer existing cloud and enterprise customers in London and Frankfurt.

Additionally, the highly experienced Zenium management team (which includes two former Sentrum execs) will be staying on after closing, giving CyrusOne a European platform with deep roots in the London and Frankfurt markets.

Easter Eggs for Christmas

CyrusOne CEO Gary Wojtaszek has been signaling for several quarters the intention to expand internationally. Dublin, the largest wholesale market in Europe, has been mentioned several times as the first likely expansion. That’s why the recent $100 million strategic investment in China's GDS Holdings, a carrier-neutral data center partner to China's large internet and ecommerce platforms Baidu, Alibaba, and Tencent, initially surprised investors.

The Zenium presentation and conference call on Dec. 21st gave CyrusOne shareholder insights into the company's expansion strategy. Investor "stocking stuffers" included:

- CyrusOne will continue to expand in Europe, either through additional platform acquisitions in top markets, or organic development.

- Amsterdam and Dublin (the largest wholesale data center markets in Europe) are on the radar screen due to faster growth rate of large-scale deployments than in secondary US markets.

- One notable exception would be the recent CyrusOne expansion into the fast-growing Atlanta market.

Additionally, there could be synergies derived from GDS’s hyper-scale customers expanding into Europe to help accelerate leasing after the Zenium acquisition closes.

Why Europe is Attractive

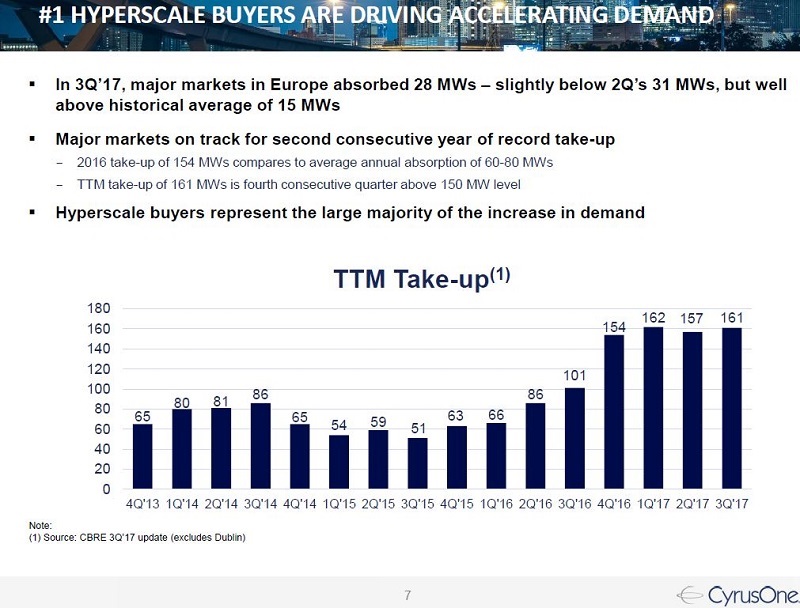

Europe is generally believed to be about two years behind the US when it comes to public cloud adoption, colocation, and enterprise application outsourcing. Pan-European retail colocation provider Interxion reported an 18 percent revenue growth rate last quarter, which is consistent with the uptick in absorption shown in the chart below:

Less than 50 percent of European data center space absorption was wholesale according to CBRE data cited in the CyrusOne presentation. This reinforces the widely held belief that large-scale colocation deployments in Europe are still in the early innings – an opportunity for CyrusOne.

Filling a Vacuum?

During the conference call, CyrusOne executives detailed how existing US cloud and enterprise clients are looking to expand into Europe. In fact, its lack of a wholesale data center offering in Europe has cost the company valuable US business when customer data center requirements were part of a global deployment, management said.

According to Wojtaszek, the European data center market lacks a "committed" wholesale developer like former US super-wholesale landlord DuPont Fabros Technology (now part of Digital Realty) and is ripe for consolidation. Wholesale development in Europe is falling to" secondary players" due to the lack of a true global hyper-scale developer he said. It is highly unlikely that Digital Realty's C-Suite would agree with that analysis. Effectively, a gauntlet has been thrown down by CyrusOne.

Digital has a much larger global footprint consisting of both wholesale campuses and retail colo data centers located in top metros across Europe. It will be interesting to see how this rivalry plays out in the region, as CyrusOne becomes active in wholesale data center development.

Paying Up for Quality Acquisitions

The number of M&A deals announced and/or consummated during 2017 highlights the intense competition for quality assets and data center businesses.

Earlier this month, Iron Mountain announced it was buying the US operations of IO Data Centers for $1.3 billion, an acquisition which will not be accretive until 2019. In a similar fashion, CyrusOne is also paying a premium to buy Zenium's data center business.

The Zenium acquisition "will be dilutive in 2018, modestly accretive in 2019, and meaningfully accretive thereafter," CyrusOne said. The 18x adjusted EBITDA multiple for Zenium considers both commenced and signed but not yet billed contracts. The midpoint of FY 2018 and FY 2019 adjusted EBITDA estimates divided by two is about $25 million.

In addition to data center assets and a European platform, CyrusOne is buying a leasing pipeline and sales funnel plus a land contract for expansion in Frankfurt. Depending upon how things play out this year this could increase shareholder returns. Zenium capex spent to support the booked-not-billed pipeline construction will be reimbursed by CyrusOne at closing.

Investor Edge

CyrusOne continues to execute on a strategic plan to become the third publicly traded US global data center player and arguably the only one with a super-wholesale focus. However, expanding into Europe requires competing head-to-head with much larger rival Digital Realty for market share.

In a sense, the Zenuim deal terms represent another gauntlet being thrown down, as the competition heats up to acquire quality data center assets and operating platforms. This is because Digital Realty CEO Bill Stein has laid out strict M&A criteria. Any Digital acquisition must be: 1) strategic, 2) immediately accretive, and 3) balance sheet neutral. Maintaining this conservative approach over time could leave Digital behind the growth curve.

Digital Realty has an investment-grade balance sheet which gives it a lower cost of capital than CyrusOne has access to. If Digital were to loosen its underwriting criteria, it could make it more difficult for CyrusOne to continue to expand. Going into 2018, investors will be watching to see if Digital Realty continues to stick to its guns or modifies its criteria.

Global interconnection leader Equinix trades at the highest AFFO multiple, giving it a distinct advantage when it comes to making acquisitions that immediately benefit shareholders. This has helped it become an M&A juggernaut. Equinix CEO Steve Smith has indicated his company would participate in the "next wave" of global hyper-scale deployments.

Meanwhile, CyrusOne is looking to become the "go-to" global wholesale data center developer through aggressive M&A and exporting its low-cost, high-speed, Massively Modular building program. Software-defined networking partners could also help CyrusOne level the playing field for global connectivity versus Equinix and Digital Realty.

As we head into 2018, it looks like a global cage match is developing between the three largest publicly traded US data center REITs, where customer relationships are likely to play a crucial role in maintaining and growing market share as global footprints continue to evolve.