Shares of colocation data center provider CoreSite Realty spiked over 5.5 percent following its strong fourth-quarter 2015 earnings report last week and upbeat 2016 guidance.

CoreSite signed more rents in 2015 than it has in any previous year and generated the highest investor returns in its sector, but the company is close to maxing out its existing building capacity in several key markets.

On the 2015 earnings call with analysts, CEO Tom Ray avoided addressing this concern in detail, saying only that the team was aware of it and “thinking accordingly.”

Record Results

While the entire data center REIT sector performed well last year, interconnection-focused CoreSite Realty delivered sector-leading 50 percent in total returns to investors.

The company saw record leasing in 2015, signing more than 500 leases totaling about 400,000 square feet of data center space, senior VP of sales and marketing Steve Smith said. Those leases add close to $50 million in rent revenue – a 40 percent increase over 2014 and the highest level of rent signed in company history.

Read more: Who Leased the Most Data Center Space in 2015?

During 2015 CoreSite added 95 new customer logos, a 16 percent year-over-year increase, including 41 net new logos for the quarter ended Dec. 31, 2015.

During Q4, CoreSite played leasing "small-ball," as Smith pointed out. Most of the 155 new and expansion leases signed in the quarter were for requirements of less than 1,000 square feet -- a 36 percent increase over the previous four-quarter average.

High Occupancy Generates High Margins

The CoreSite mid-to-high-teen ROIC is derived in no small part from building out existing powered shell space. An analyst pointed out on the call that CoreSite was now building out the final phases, and capacity will be maxed out in both Chicago and Northern Virginia markets.

Ray confirmed that there has been a noticeable increase in interconnections between enterprise customers and cloud providers. Additionally, CoreSite saw growth of these interconnections increasing at a faster rate in 2015, compared with the rate of increase reported in 2014.

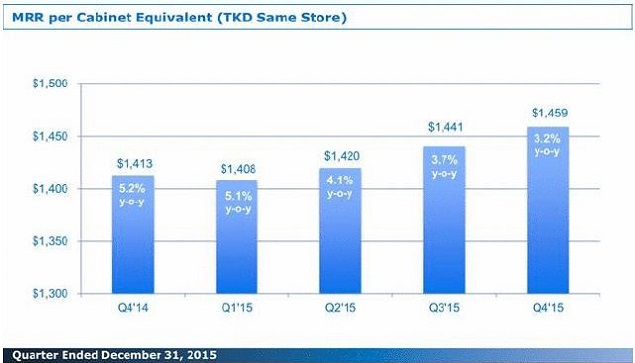

CoreSite's monthly recurring revenue per cabinet over the last five quarters (Source: CoreSite Q4 2015 Supplemental)

Something Investors Should Consider

When it comes to allocating capital to drive strong near-term results, the correct answer will almost always be to build out existing properties. CoreSite will continue to deliver great numbers leasing to sub-1,000-square foot tenants in existing powered shell space. However, they are currently developing the final phases in two of the strongest Tier I data center markets.

Notably, the highest returns are usually associated with the final phases of any data center development -- especially when compared with the costs associated with delivering the first phase of a new project. The question investors should be asking is: What happens when most of the low-hanging fruit has been harvested?

While this is a challenge facing the company moving forward, it comes as no surprise that the CoreSite management team refused to spill any candy, or tip their hand on the call.

Read more: Things Data Center Investors Should Know

Key Earnings Call Takeaways

Best Markets: The strongest leasing markets in Q4 for CoreSite were Los Angeles, the Bay Area, Chicago, and Northern Virginia. Together, these four markets accounted for 80 percent of new and expansion leases signed in Q4 and 95 percent of annual GAAP rent for the quarter.

Booked, not Billed: CoreSite reported signed but not yet commenced leases of $15.9 million as of December 31, 2015, or $27.2 million on a cash basis.

Interconnection Trends: interconnection revenue growth for the fourth quarter was 26 percent over the same quarter in 2014, with calendar 2015 reflecting 25 percent growth over 2014 results. Notably, while growth in copper cross connection revenue weakened, growth in fiber cross connections remained strong in 2015.

CoreSite reported 50 percent growth in its "higher value" logical interconnection products, comprised predominantly of its Any2 Internet exchange, blended IP, and the CoreSite open cloud exchange.

Development: In the fourth quarter, CoreSite had a total of 370,000 square feet of capacity under construction consisting of both turnkey data center and powered shell space. This included projects underway in Santa Clara, Northern Virginia, Boston, and Los Angeles.

Deferred Expansion Capital: CoreSite now reports CapEx required to fully build out the space in accordance with its plans to add full capacity to its data centers as a separate line item. Notably, the total budgeted amount of $30 to $40 million may not actually be spent.

Investor Takeaway

CoreSite scored points with investors when it came to the REIT metrics that really matter. The data center REIT reported year-over-year Funds from Operations growth of 31 percent and grew the annual dividend by 26 percent.

CoreSite introduced 2016 FFO guidance of $3.37 to $3.47 per diluted share, which implies a 20 percent increase over 2015 FFO of $2.86 at the midpoint.

Denver-based CoreSite has now closed out the books on a "winning season" for 2015, both for the company and for the Denver Broncos, the Super Bowl 50 champion.

The focus now should be on acquiring what these teams need to succeed next season.